The G20/OECD BEPS Project Action 11 report, Measuring and Monitoring BEPS, included a number of insights beyond the widely reported annual global revenue loss range of US$100-240 billion in 2014. One analysis showed that while the average OECD corporate tax rate was declining, tax rate differentials between OECD countries were increasing. So the incentives for profit shifting was increasing, not decreasing.

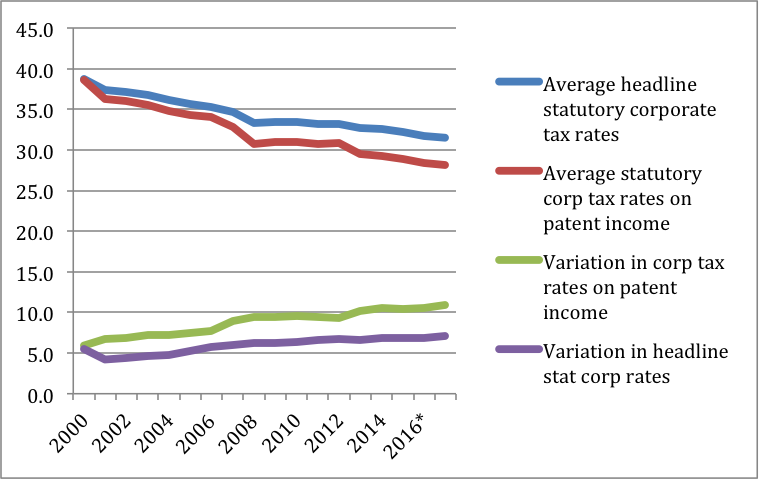

The trend of increasing tax rate differentials among OECD countries, despite decreasing average corporate statutory or “headline” tax rates, has continued to grow into 2017. The above chart uses an average OECD rate, weighted by Gross Domestic Product (GDP), unlike many analyses using unweighted averages that give Estonia the same weight as Germany. The chart presents both the top (“headline”) corporate statutory marginal tax rate as well as special lower tax rates on certain patent income (“patent or innovation boxes”). The tax rate differential is measured by the standard deviation of tax rates around the weighted mean. The Action 11 report found similar trends using Foreign Direct Investment and cross-border trade.

The weighted-average headline OECD corporate tax rate has fallen from 38.7% in 2000 to 31.5% in 2017, while the average tax rate on intellectual property (IP) income has fallen from 38.6% in 2000 to 28.1% in 2017. Meanwhile, the variation in headline corporate rates increased from 5.5% in 2000 to 7.1% in 2017, and the variation in patent income tax rates increased from 5.9% in 2000 to 10.9% in 2017.

Lower weighted-average statutory corporate tax rates reduce the tax rate differential with zero corporate rate tax havens, but havens’ importance to GDP is minimal, and the incentive to reach a 0% rate is still strong whether from the US headline rate of 39% or Ireland’s rate at 12.5%.

The U.S. is a big part of the profit shifting story, but not the only part. The BEPS Action 11 report highlighted many empirical studies that found significant profit shifting among non-US companies. If the U.S. lowered its combined federal and state corporate headline rate to 25%, the average OECD rate would decline to 26.1%, and the tax rate variation would fall to 4.0%, below the variation in 2000. A 25% US combined rate would be lower than the GDP-weighted average of the other OECD countries by 1.8 percentage points.

It should be noted that the variation in “headline” corporate tax rates between non-US OECD countries declined over the 2000-2017 period along with their average tax rate. Tax rate differentials between non-US OECD countries and also tax havens continue to incent non-US companies to profit shift.

As long as country sovereignty in setting their tax rates and origin-based corporate income taxes remain fundamental building blocks of corporate income tax systems, governments will need to use tax systems (non-tax rate/base) measures, such as the anti-BEPS measures proposed in the BEPS project to reduce harmful tax competition between countries and to minimize tax-induced profit shifting by MNEs.

Tom Neubig