The IRS Statistics of Income Division just released its biannual US Controlled Foreign Corporation (CFC) data for 2016. US multinational corporations are required to file Form 5471 for each CFC noting the country of incorporation, assets, receipts, earnings and income taxes paid. Sixteen thousand US corporations had 95,000 CFCs with earnings of $1.07 trillion in 2016.

The change in US CFC tax return data between 2014 and 2016 provides some empirical evidence of whether the G20/OECD Base Erosion and Profit Shifting (BEPS) project changed some US MNEs’ tax-planning behaviors. The final BEPS reports were published in October 2015, and four minimum standards including Country-by-Country Reporting (CbCR) rules for large MNEs would have been fully anticipated in the 2016 filings. Some contemporaneous tax director surveys reported that US MNEs were changing some of their international tax planning and operations, such as increased focus on reputation risk and curtailing so-called “cash boxes,” as cited by the OECD report to the G20 Leaders in July 2017.

Although the BEPS four minimum standards and the revised transfer pricing guidelines were not expected to significantly affect US MNEs, given extensive US transfer pricing regulations and Form 5471 reporting, changes in US MNE tax activity might become apparent comparing Form 5471 reporting in 2014 with the reporting in 2016. Some MNEs might have “cleaned up” their global operations shedding some tax haven subsidiaries in anticipation of CbCR reporting. Some MNEs might have shifted income away from “cash boxes” to other countries with low tax rates but with real economic activities.

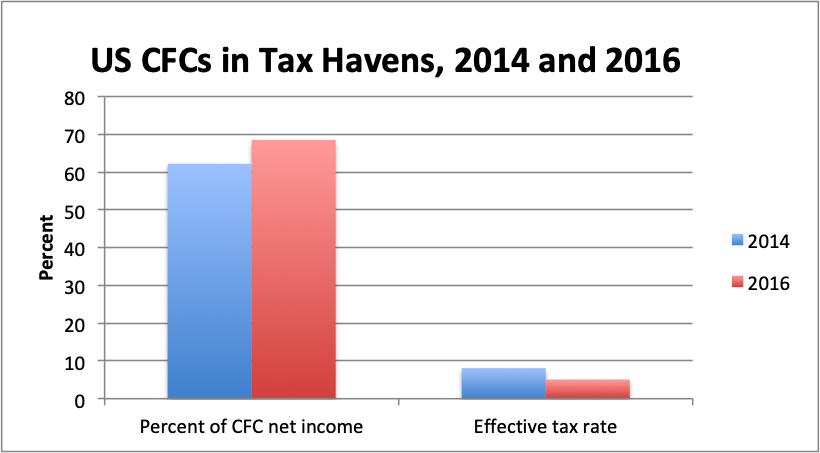

The 2016 US CFC tax return data do not appear to show a significant reduction in BEPS in terms of measures of income earned in countries that have been labeled “tax havens” and the effective tax rates on that income. Between 2014 and 2016, the share of CFC income actually increased from 62% to 68% in nine “tax haven” countries (Bahamas, Bermuda, British Virgin Islands, Cayman Islands, Ireland, Luxembourg, Netherlands, Singapore and Switzerland). $733 billion of the total $1,070 billion earned by US MNEs’ CFCs were earned in those countries. The effective tax rates on the income earned in those countries declined from 8.1% in 2014 to 5.1% in 2016. Some compositional change in tax haven locations may be occurring, as shown in the table below, but may be due to non-tax factors.

Implementation of BEPS was still occurring in 2016 in many countries, along with the European Union’s Directive on Anti-Tax Avoidance. National legislation was required for implementation of many of the anti-BEPS provisions with future effective dates. Thus, 2016 may be too early for significant anti-BEPS changes in US MNEs’ behavioral effects. Major changes in US international and corporate tax rules in December 2017 are expected to reduce profit shifting from the U.S., including the reduction in the US corporate tax rate from 35% to 21% and the introduction of the GILTI (minimum tax rate on foreign income) provision.

Release of US CbCR 2017 data, the first year of mandatory reporting, is expected in December 2019. The OECD Corporate Tax Statistics publication of many other countries’ aggregated CbCR tabulations is expected early in 2020. This additional data will provide a baseline from which to measure anti-BEPS effects going forward. A two-year wait for 2018 US CFC data reflecting full implementation of the BEPS project and the significant US tax changes will seem like an eternity.

Tom Neubig