The IRS Statistics of Income released the 2017 Country-by-Country reports (CbCR), a major transparency initiative of the OECD/G20 Base Erosion and Profit Shifting (BEPS) project. The 2017 data is the first year of mandatory reporting by US MNEs.

The 2017 CbCR reports provides important aggregate tabulations of US-headquartered MNEs operations globally, for those with over $850 million of total revenues. The CbCRs are designed to assist tax administrations more effectively audit MNEs to identify BEPS behaviors. The aggregate tabulations will help policy analysts analyze global tax reforms, such as Pillar 2 global minimum tax proposal being considered by the OECD/G20 Inclusive Framework on BEPS in their work addressing the tax challenges of the digitalisation of the economy.

2017 aggregate tabulations. 1,575 US MNE groups filed 2017 CbCRs with the IRS, most reported activity in the United States. In 2016, 1,101 MNE groups voluntarily filed CbCRs. Comparisons between 2016 and 2017 are therefore difficult due to different years as well as a different group of MNEs.

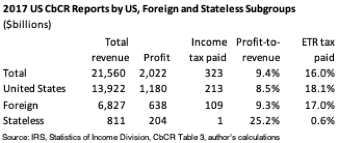

The large US MNEs reported $2.0 trillion of profits on $21.6 trillion of total revenues, $323 billion of income tax paid and $376 billion of income tax accrued. The average profit rate on revenue was 9.4% with an effective tax rate of 16.0%. Roughly two-thirds of the revenue, profit, and income tax paid was in the United States. US subgroup activity had slightly lower profitability rates (8.5% compared to 9.3% for foreign) and slightly higher effective tax rates (ETR) on tax paid (18.1% compared to 17.0% for foreign). “Stateless entities” had an average 25% profit rate and a corporate ETR of 0.6%.

In 2017, 620 “stateless entities” filed CbCRs. Many of these are “fiscally transparent” enterprises, such as partnerships and Limited Liability Corporations (LLCs), which are taxed at the owner level, rather than at the corporate or entity level. They reported $204 billion of profits, or about 10% of total profits reported by large US MNEs. Some “stateless entities” may be corporations, such as reverse hybrids, that would pay corporate income tax, except for tax planning. Separating these two types of “stateless entities” would assist in better understanding the data.

Effective tax rates. The IRS published the distribution of effective tax rates (income tax accrued divided by profits) of MNE subgroups. Subgroups are “constituent entities” (affiliates) that have tax jurisdiction in the same country. The 1,575 reporting MNE groups have 35,008 subgroups, of which 11,055 have negative or zero reported profits. Roughly 24,000 subgroups reported $2.4 trillion of positive profits. Subgroups with ETRs of less than 5% (including negative tax with positive profit) accounted for 47.5% of total positive profits. Subgroups with ETRs less than 10% accounted for $1.36 trillion or 56.5% of total positive profits. Some of these low ETR subgroups could be partnerships or other entities taxed at the owner level, but since stateless entities only accounted for $215 billion of positive profits, almost half of total positive profits were subject to tax rates below 10% for US MNE corporations.

If a minimum tax of 10% had been imposed at the subgroup level (“country-blending”) on these large US MNEs, it would have raised $107 billion in 2017 on a static basis. Some of the low-ETR subgroups will be subject to the 2017 tax legislation GILTI-provision, although that is done at an overall consolidated group level basis. The reported ETRs may be understated due to inconsistency in how intercorporate dividends are reported due to lack of guidance on whether they should be excluded from profits. Going forward, intra-corporate dividends will be excluded from reported profits.

The IRS release of the 2017 CbCR includes a lot more information about US MNE’s operations, profits and taxes across countries and across industries. More analysis of the new data is needed.

Some next steps. The OECD will be publishing a number of other countries’ CbCR aggregate tabulations, similar to the US tabulations, in a forthcoming OECD Corporate Tax Statistics report. The CbCR tabulations will be helpful in the analysis of the Pillar 2 global minimum tax proposal. Aggregate tabulations of the CbCR data will be new data for many other countries, which don’t have the US equivalent of the Form 5471 tabulations and the BEA’s Activities of Multinational Enterprises tabulations for US MNEs.

CbCR data provide the IRS and other tax administrations with additional information beyond the data reported on the Form 8975. A report by the IRS on how CbCRs are helping improve their audits of MNEs would be useful. The SOI is also using academic tax researchers to help analyse the data on a micro basis, although all tabulations will be aggregated and anonymized, but such analysis will likely provide additional insights on key relationships.

Additional information about foreign-headquartered MNEs operating in the U.S., beyond the Form 5472 data, will become available with the reporting of other countries’ CbCR tabulations. Analysis of that data, while incomplete, will supplement the tabulations from US MNEs.

Finally, the BEPS Action 13 report calls for a reevaluation of the CbC reporting in 2020. Input from tax administrations’ use of the individual CbCRs as well as tax policy analysts’ use of the aggregate tabulations should inform changes to the CbCR data template as well as the extent to which more publicly available data from the CbCR would be desirable.

Tom Neubig