IRS released aggregated Country-by-Country Reporting (CbCR) data from large US-headquartered multinational enterprises (MNEs) from 2016, the initial year of the OECD/G20 BEPS transparency implementation. [Link] The six tables provide a first look at CbCR data from US MNEs, which show some of the insights as well as limitations of the reported data.

1,101 US corporations and partnerships filed Form 8975 for 2016. Additional US MNEs are expected to file in 2017, the first year of mandatory reporting. The reporting MNEs had global revenue in excess of $850 million. The US ultimate parents had 26,473 constituent entity subgroups in separate jurisdictions. The total number of constituent entities was 154,000, with roughly 54,000 entities in the US and 100,000 entities outside the US. Given the aggregation in the CbCR template, multiple entities in a single country are combined into subgroups for reporting purposes. Form 8975 data filed by 14 foreign controlled domestic corporations are not included in the tables.

As the OECD/G20 BEPS Action 13 states: “The Country-by-Country Reports will be helpful for high-level transfer pricing risk assessment purposes.” It goes on to say: “It may also be used by tax administrations in evaluating other BEPS related risks and where appropriate for economic and statistical analysis.” The IRS should be commended for releasing these aggregated tabulations, prior to the inclusion in a forthcoming OECD Corporate Statistics publication with other countries’ CbCR data. With the consideration of revised profit allocation and nexus rules and a global anti-base erosion proposal [Link], the CbCR data will provide significant incremental insights into MNEs’ business and tax activities.

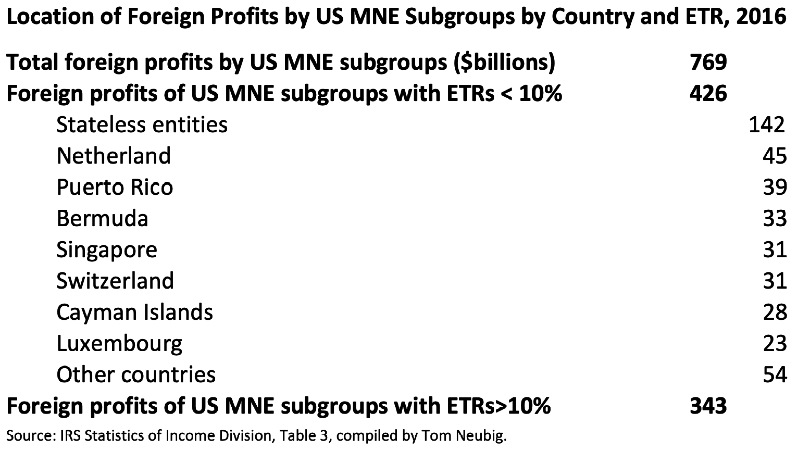

Effective Tax Rates. The table below shows 950 US MNE groups had 4,246 subgroups in jurisdictions with positive profits yet effective tax rates less than 5%. These subgroups accounted for 18% of revenue, 48% of net profits, and only 3% of income tax accrued. $689 billion of profit was earned by profitable MNE subgroups with ETRs less than 5%. Their profits were 24% of their total revenue and 52% of their tangible assets.

322 (or 29%) of the MNEs groups reported profitable “stateless entities” which earned $142 billion of income (18% of total non-US net profit) and paid only $700 million in foreign income tax (an effective tax rate of 0.6%). The OECD instructions required a separate line for all constituent entities in a MNE group deemed by the reporting MNE as not resident in any tax jurisdiction for tax purposes. These include “fiscally transparent” entities or “ghost companies,” such as Apple Sales International that earned tens of billions of income not reported to any tax authority several years ago since it was incorporated in Ireland but managed and controlled from the U.S. The CbCR data reports over 10,000 stateless entities controlled by US MNEs. Some of the stateless entities are pass-through partnerships that are not subject to corporate tax but are owners are subject to personal income tax, while others are “reverse hybrids” with significant untaxed income.

Domestic vs. Foreign Activity. The CbCR data includes parents and domestic affiliates in the US as well as US MNEs’ subsidiaries and branches in other countries. The table below shows the largest US MNE’s for their profitable entities reported 65% of their revenue as received in the US and 56% of their total profits earned by US entities. [84 of the 1,101 US MNEs did not report activity in the US, which is likely a data issue in the first, voluntary year of implementation, but which would overstate non-US activity since calculated as All Jurisdictions less U.S..] The profitability of the US entities was lower than their non-US entities. The ratio of profit to total revenues was 10.5 for US entities versus 15.5% for their non-US entities. The ratio of profit to tangible assets was 27.8% for US entities versus 52.8% for non-US entities. One cause of that difference is likely the shifting of intangible assets out of the US to jurisdictions with lower tax rates. In addition, the ETR for US entities was twice that of the non-US entities (18.9% and 9.6%, respectively).

CbCR vs. Other MNE Data. US government data on US multinationals has been extensive and best in class, so the CbCR reports will be most helpful in other countries. The US publishes tax return data from the Form 5471 from Controlled Foreign Corporations. [Link] The US Bureau of Economic Analysis publishes data on the Activities of Multinationals Enterprises (AMNE). [Link] The table below shows selected comparisons of the Form 5471 data (from 2014) and the Form 8975 data (from 2016). Since only MNEs with global revenues exceeding $850 million file the Form 8975, the total amounts reported on the Form 8975 are lower. The relative effective tax rates for the Caribbean island havens and Ireland are flip-flop, likely due to different years, different MNEs included, or different reporting measures.

Academics have noted the concentration of foreign income of US MNEs from Caribbean islands, Ireland, Luxembourg and Switzerland, accounting for 63% of total foreign income from the BEA AMNE (2016) and 59% of total foreign income from the Form 5471 (2014). The CbCR data show only 24% of total foreign income from those countries as reported by the largest US MNEs in 2016. Reasons for the difference are worth pursuing as well as reasons for the negative net income reported from US MNE affiliates in Luxembourg and Switzerland.

Opportunities. The new CbCR data provides some important insights into the business and tax activities of the largest MNEs. Tax administrations will be able to use it for high-level transfer pricing enforcement, more efficiently identifying issues for further examination. Statistical and economic analysis of the aggregated data will help policymakers and policy analysts understand additional dimensions to MNE activity, such as stateless entities and low ETR entities. For example, estimates of so-called residual profits in excess of a return on tangible assets (similar to the new U.S. Global Intangible Low Taxed Income provision) can be calculated.

As more analysts examine the new US CbCR data tabulations additional insights as well as questions for further data collection and analyses will emerge. As CbCR data for other countries are tabulated and published by individual countries or the OECD, it will be important to determine if stateless entities and low ETR entities are as prevalent in non-US MNEs. They will also provide additional information to supplement the IRS Form 5472 data on foreign-owned US corporations.

Limitations. Aggregated tabulations limit the number of dimensions that can be explored analytically. Due to confidentiality issues, other countries will not be able to provide the same granular detail as the U.S. with its 1,101 ultimate parents reporting. The US CbCR data fortunately included tabulations for profitable entities, rather than limiting tabulations to net income (profit less losses), which is not a good a measure of taxable income.

The new data is for a snapshot in time. It will be important to use the CbCR data to analyze changes over time as the BEPS minimum standards and national anti-base erosion rules take effect. For example, what would the data have shown in 2013 before the BEPS Project and the anticipation of such transparency?

Aggregated results can prevent accurate measurement of distributions, such as low ETRs. For example, the ETR tabulation reports that $689 billion of income was subject to an ETR of less than 5%. By contrast, tallying the country distribution of profitable entities with an average ETR of less than 5% results in only $318 billion since entities with low ETRs are located in countries with higher average ETRs.

The data does not help analysts understand why ETRs are low or high. Low ETRs could be due to low statutory tax rates, special deductions or exemptions, tax credits, or aggressive tax planning. Additional analysis with other data is needed.

In addition to uncertainty about the composition of “stateless entities” between pass-through entities vs. zero-taxed hybrid entities, the CbCR data may include some double counting of inter corporate dividends. Income from lower-tier subsidiaries distributed as dividends to higher-tier entities may also be included by the higher-tier entities.

The revenue data is helpfully broken out between third-party and related-party revenue, but the revenue is origin-based, not destination-based. The revenue is from the location of the entity selling the product or service, not where the final consumers are located.

Progress. Kudos to the IRS Statistics of Income Division for its timely release of the initial US Country-by-Country Report tabulations with tabulations helpful to both tax administration and tax policymaking. The OECD/G20 BEPS Action 13 Transfer Pricing Documentation and Country-by-Country Reporting is now a minimum standard of the 129-member BEPS Inclusive Framework. The increased transparency of MNEs’ business and tax activities is a significant step forward in reducing tax-induced profit shifting. I look forward to the release of other countries’ CbC reports and future years’ reports to track changes in BEPS over time.

Tom Neubig